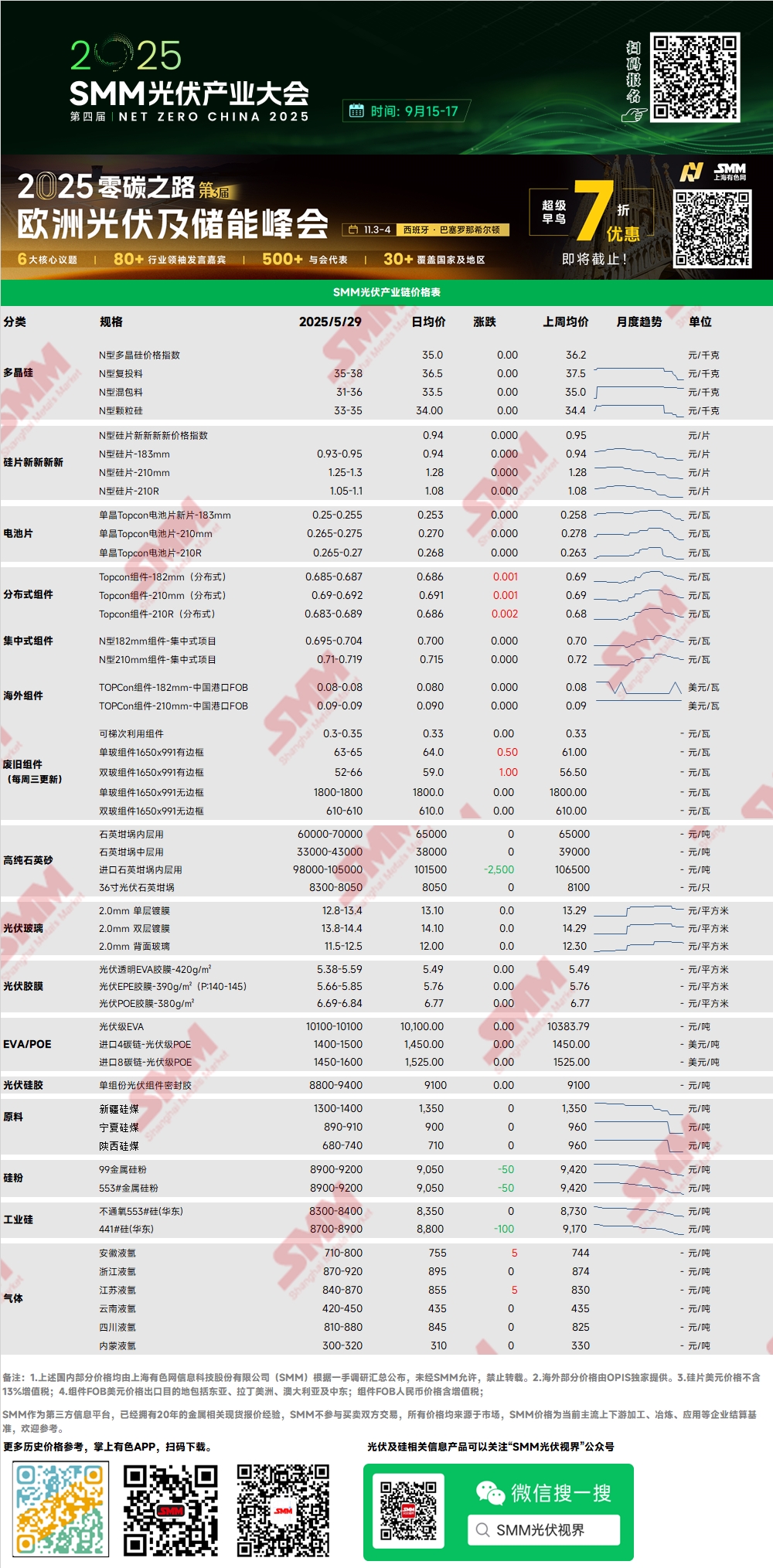

Polysilicon: This week, the price index for N-type polysilicon was 35.01 yuan/kg. The price of N-type recharging polysilicon ranged from 35-38 yuan/kg, while the price of N-type mixed polysilicon was 31-36 yuan/kg. Overall, polysilicon prices remained largely stable. Polysilicon transactions this week were relatively limited compared to last week, with downstream inventory levels being sufficient and procurement enthusiasm weak. Polysilicon production schedules for June are expected to increase slightly, involving production increases/resumptions at 2 bases and production cuts/shutdowns at 3 bases. Polysilicon production operations are weaker than previously expected, with overall resumptions during the rainy season being cautious.

Wafer: This week, the price of N-type 183mm wafers ranged from 0.93-0.95 yuan/piece, 210R wafers were priced at 1.05-1.1 yuan/piece, and 210mm wafers were priced at 1.25-1.3 yuan/piece. Wafer prices remained stable overall, with major manufacturers' quotes gradually stabilizing at 0.93 yuan/piece. Currently, cost losses are widespread among wafer enterprises, and the market is gradually approaching a low point, with limited price declines. In June, a relatively large number of wafer enterprises are expected to reduce production, with this situation being widespread, but the extent of reduction for each enterprise is limited. It is anticipated that wafer production will decline in June, but the decline will be narrow.

Cell: Compared to last week's prices, the market for cell sizes has become increasingly differentiated. The price of 183N cells continued to decline WoW, with mainstream transaction prices generally reaching 0.25 yuan/W, reflecting weak end-use demand. Domestic orders have contracted significantly, while overseas orders have remained relatively stable. The price of 210RN cells remained stable, with the bottom transaction price closing above 0.265 yuan/W, supported by demand, resulting in relatively firm pricing. The price of 210N cells declined WoW, mainly due to price competition, with the transaction price of 0.265 yuan/W falling below historical lows. This week's cell price trends fully reflect the structural changes in downstream demand. Faced with this situation, some producers have initiated or plan to upgrade their existing 183 production lines to expand 210RN and 210N capacity, aiming to match the existing demand in June and accelerate cash flow recovery to ensure operational continuity. Looking ahead to June, it is expected that the production schedule for solar cells will tighten. However, whether the competitive pressure in the cell segment can be alleviated hinges on the comparison between the extent of production tightening in the cell segment and that in the downstream module segment, namely, the marginal changes in the supply-demand relationship.

Module: This week, PV module prices first declined and then rose. The mainstream transaction price for N-type 182mm modules in centralized projects ranged from 0.695-0.704 yuan/W, with the average price declining by 0.14%. The mainstream transaction price for N-type 210mm modules ranged from 0.71-0.719 yuan/W, with the average price also declining by 0.14%. The price of distributed N-type 182mm modules was around 0.685-0.687 yuan/W, with the average price declining by 0.44%. The price of distributed N-type 210mm modules was 0.69-0.692 yuan/W, with the average price declining by 0.43%. The price of distributed N-type 210R modules was 0.683-0.689 yuan/W, with the average price increasing by 0.29%. This week, it was learned that there were isolated cases of "installation rush after procurement" by some local governments. However, the overall decline in distributed PV orders was significant. At present, module inventory turnover is relatively healthy, so selling prices and profit margins are relatively optimistic. Subsequent attention will focus on whether module companies will significantly reduce prices after production cuts. Overseas, the European Net-Zero Industry Act (NZIA) announced new regulations aimed at stimulating local manufacturing, which will impact 30% of domestic export orders to Europe in 2026. Due to the act, a small-scale installation rush may occur in Europe in H2.

Terminal: From May 19, 2025, to May 25, 2025, SMM statistics showed that domestic enterprises won a total of 27 PV module projects. The winning bid prices for PV modules were concentrated in the range of 0.66-0.82 yuan/W, with a weekly weighted average price of 0.04 yuan/W. The average winning bid price for the week was 0.73 yuan/W, an increase of 0.02 yuan/W compared to the previous week. The total procurement capacity of winning bids was 830.04 MW, an increase of 800.49 MW compared to the previous week.

Film: The mainstream price range for EVA film is 13,000-13,200 yuan/mt, and the price range for EPE film is 14,500-15,000 yuan/mt. On the cost side, the price of PV-grade EVA has pulled back, providing cost support for the downward movement of film prices. On the demand side, affected by the decline in module prices, demand is weak. New order prices for film in June are expected to decline.

EVA: This week, the price of PV-grade EVA was in the range of 10,100-10,400 yuan/mt, with the transaction center continuing to pull back. Demand for foam-grade and cable-grade EVA has slowed down, and prices have also declined significantly. On the demand side, there is an expectation of downward new order prices for film in June, with weak demand. The transaction pace in the EVA market has slowed down, with overall transactions being average. Film companies have a strong wait-and-see sentiment. It is expected that EVA prices will still be under pressure.

POE: The domestic delivery-to-factory price of POE remains stable at 12,000-14,000 yuan/mt. Under the dual pressures of gradually weakening demand and the successive release of new capacity, it is expected that the price of PV-grade POE will be under pressure.

PV Glass: This week, quotes from some PV glass companies continued to decline. As of now, the mainstream quote for 2.0mm single-layer coated PV glass in China is 13.0 yuan/m², with some companies' quotes dropping to 12.8 yuan/m². The mainstream quote for 3.2mm single-layer coated PV glass is 21.0 yuan/m², and the mainstream quote for 2.0mm back-coated glass is 11.8 yuan/m². This week, the quote center for the domestic PV glass market has pulled back. As of now, the quote for 2.0mm single-layer coated PV glass is 12.8-13.4 yuan/m². At the end of May, leading module companies began to enter the market for procurement. To compete for orders, glass companies have accelerated the pace of price reductions in recent days. The market atmosphere is highly competitive, with transaction prices falling rapidly. Some transaction prices have dropped below 13 yuan/m². SMM expects that prices for new orders, especially in June, will continue to decline. The decline in module production schedules is the dominant factor, while the accelerated release of production on the supply side is quickening the pace of supply surplus.

High-purity quartz sand: This week, the quoted prices for some domestic high-purity quartz sand products continued to decline. The current market quotes are as follows: Inner layer sand is priced at 60,000-70,000 yuan/mt, middle layer sand at 33,000-43,000 yuan/mt, and outer layer sand at 17,000-24,000 yuan/mt. Prices dropped slightly, with domestic sand prices fluctuating at the lower end this week. Domestic sand enterprises are under significant pressure due to the combined effects of weakened downstream demand and the downward trend in downstream crucible prices. Meanwhile, recent negotiations on imported sand prices have achieved new breakthroughs, and imported sand prices are expected to fall. Domestic sand enterprises' refusal to budge on prices is once again facing challenges, leading to a slight decline in sand prices recently. Regarding the price forecast, influenced by the overall weakness of the PV market and the supply surplus of sand enterprises, sand prices are expected to continue to decline. However, due to the limited inflow of imported ore sources recently, there is still support at the lower price levels, and the decline is expected to be limited.

》View the SMM PV Industry Chain Database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)